A periodic inventory system is a simple and economical way to keep track of inventory levels and costs. It requires less effort to set up and maintain than other inventory systems, making it an attractive option for many businesses. In periodic inventory, only the time records at the start and end of the period are entirely correct. A company relies on predictions of its present inventory levels for the remainder of the time. One may lose sales and customers if inventory is too low or if an unnoticed inventory discrepancy in the accounts.

Sale of Merchandise

Periodic inventory is the inventory control system that does not keep track of the inventory balance and cost of goods during the month. The possibility of a human mistake increases when you physically count all the inventory goods you have on hand. After taking stock of all inventory, look for anomalies or statistics that seem noticeably higher or lower than anticipated to avoid this. This indicates that other techniques are more appropriate for businesses with a high inventory turnover rate, a high number of SKUs, demands for multichannel inventory management, or who want real-time data. Generally Accepted Accounting Principles (GAAP) do not state a required inventory system, but the periodic inventory system uses a Purchases account to meet the requirements for recognition under GAAP.

Which Companies Use The System?

Many small firms have inventory management systems connected to their POS or online store. The inventory is automatically updated when the cashier scans a barcode, and a customer leaves with a purchase. When a instructions for form 5695 sales return occurs, perpetual inventory systems require recognition of the inventory’s condition. Under periodic inventory systems, only the sales return is recognized, but not the inventory condition entry.

Different between Periodic and Perpetual

Businesses frequently mix the two accounting techniques to manage inventory. The cost of products sold and the precise amount of goods in inventory are typically unknown to businesses using the periodic inventory method until a physical count is done. For this reason, the system is advised for companies with a limited number of SKUs operating in a market that moves slowly. With successive journal entries, all other entries are connected to the accounts for purchases and payables. It enables them to accurately reflect the expenses of the cost of the items offered.

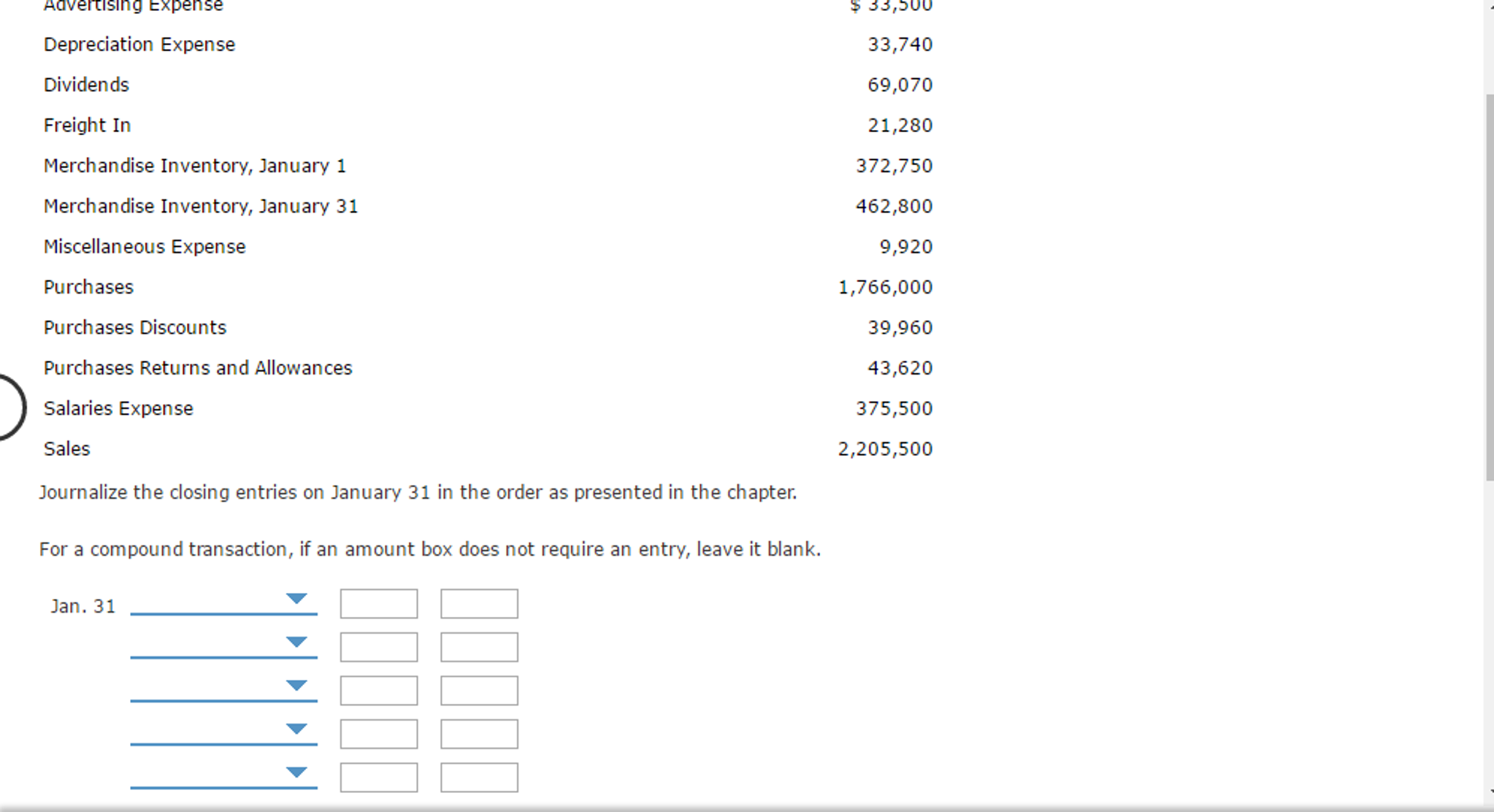

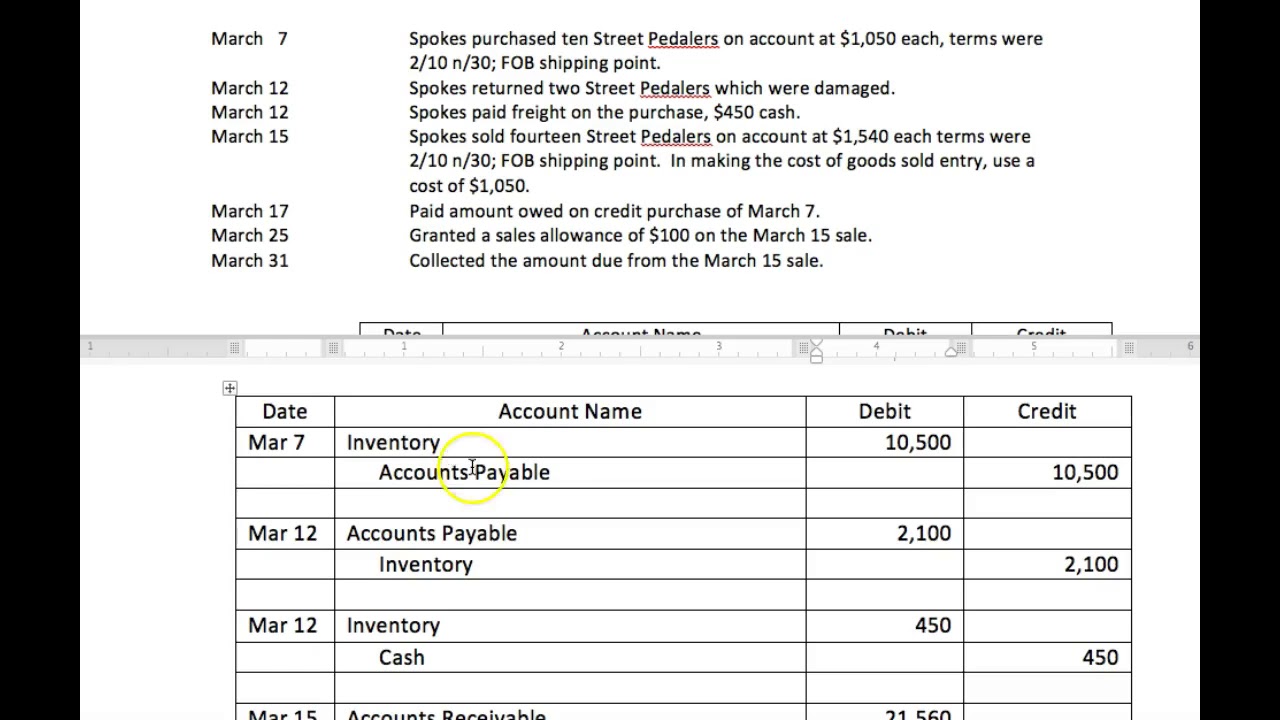

In a periodic inventory system, journal entries for purchases and sales do not directly affect inventory until the end of the period, when COGS is calculated and recorded based on the physical count. This method simplifies daily record-keeping but requires a thorough physical count to ensure accurate financial reporting. At the month-end, company will perform an inventory physical count and record it into the financial statement. The purchase account will be reversed to zero alongside with previous month’s balance.

You can calculate the COGS by using a balancing figure or the COGS formula. In this entry, the debits are in the ending inventory rows and the COGS row, and the credits are in the beginning inventory and the purchases rows. Get an accurate view of your company’s financial health with Skynova’s all-in-one invoicing and accounting software. Check your income and expenses in real time for better-informed business decisions.

A periodic inventory system is an approach businesses can use to evaluate their merchandise inventory and the cost of goods sold. At the end of the accounting period, you need to determine your firm’s actual ending inventory and “cost of goods sold.” At first, his $100 will be shifted from Purchase Account to Inventory Account. This purchase account can be a temporary account to hold all the inventory purchases for a given accounting period.

- A contra account is meant to be opposite from the general ledger because it offsets the balance in their related account and appears in the financial statements.

- LIFO means last-in, first-out, and refers to the value that businesses assign to stock when the last items they put into inventory are the first ones sold.

- Now, keep in mind that the previously mentioned advantages only benefit small businesses that deal with a couple of hundred sales a year.

A perpetual system can scale, so whether you have five products (today) or 200 products (tomorrow), a perpetual system can effectively manage inventory control. Periodic inventory is an accounting stock valuation practice that’s performed at specified intervals. Businesses physically count their products at the end of the period and use the information to balance their general ledger. This system allows the company to know exactly how much inventory they have at any specific time period.

Overall, the perpetual inventory system is superior because it tracks all data and transactions. However, with a perpetual system, you need to make more decisions to use it successfully. Since the specific identification method, identifies exactly which cost the purchase comes from it does not change under perpetual or periodic. Under the perpetual method, cost of goods sold is calculated and recorded with every sale.

A periodic inventory system also requires manual data entry and physical inventory counting. A periodic Inventory System is defined as an inventory valuation method in which inventories are physically counted at the end of a specific period to determine the cost of goods sold. That means ending inventory balance is updated only at the end of the period instead of a perpetual inventory system where inventories are counted frequently. Conducting regular physical counts of stocks is an essential part of verifying and maintaining accurate inventory records. Companies need to take into account the stock levels of their products in order to plan for future orders and to ensure that their records are always up-to-date.

Instead, these items are determined at the end of each quarter, year, or accounting period. Sales Return and Sales Discount is the contra account of sales revenue, so it simply reduces the sale amount from income statement. In a periodic inventory system, inventory tracking is manually updated at the conclusion of a certain period. Through point-of-sale inventory systems, the perpetual inventory system keeps track of inventory by immediately documenting any alterations.